In accordance with the provisions of UCP 500, the terms "documentary credit" and "standby letter of credit" mean any arrangement where a bank, acting at the request of a customer, is to make payment to a third party (the "beneficiary"), or authorizes another bank to make such a payment. The letter of credit can also:

• be put in place by the bank acting on its own behalf;

• be made payable to the order of the beneficiary;

• require the bank to accept and pay bills of exchange (drafts) drawn bythe beneficiary; and

• require the negotiation of payment, or acceptance, against the presentation of stipulated documents by the beneficiary.

Separation of letters of credit and commercial contracts

Letters of credit used to pay for the export sale are separate from the underlying commercial contract between the Korean exporter and the foreign buyer. This is a valuable feature in making the payment under the letter of credit secure as the foreign buyer cannot use a claim of non-performance under the commercial contract to stop payment to the exporter. This separation of commercial contract and letter of credit also means that the bank does not attempt to satisfy itself that the terms of the commercial contract have been fulfilled. Rather, the bank looks solely to the documentary requirements of the letter of credit and whether they have been perfectly satisfied when determining whether to make payment under the letter of credit. Normally, the bank cannot make payment under the letter of credit if the documents are not in order, even if the exporter has essentially satisfied the terms of the commercial contract. In this latter regard, the exporter's bank may be willing to advance funds under the letter of credit to the exporter against discrepant documents against the exporter's guarantee of reimbursement to the bank if the foreign buyer's bank is unwilling to reimburse the exporter's bank because of the discrepancies in the documents.

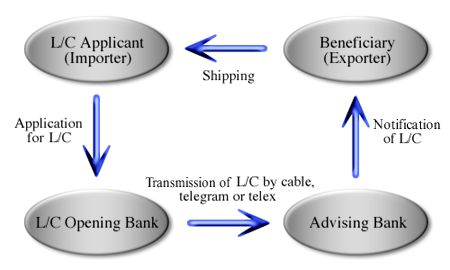

Letter of credit issuance process

The letter of credit issuance process involves four key parties: the foreign buyer, the foreign buyer's bank, the exporter's bank, and the exporter. Under UCP 500, these parties are called "the Applicant," the "Issuing Bank," the "Advising (or Letters of Credit Confirming) “Bank and the Beneficiary” Additional parties, the so-called "Nominated Paying/Negotiating/Accepting Bank" and the "Transferring Bank," may be added to the process. This can occur if: (1) the advising (or confirming) bank is located too far away from the exporter to conveniently process the documents and effect payment, negotiation of documents, or acceptance of the bill of exchange; or (2) a transferring bank is required to assist in the transferring of documents and payments between the advising (or confirming) bank and the issuing bank. However, the process is usually a bit simpler, as the advising bank may also be nominated to be the confirming and/or paying, accepting, or negotiating bank. Also, if the letter of credit is "freely negotiable" any bank is a nominated bank for purposes of processing the letter of credit. It is important to note that the advising or confirming bank processing the letter of credit with the exporter need not be the exporter's regular commercial bank.

The process begins as the exporter and foreign buyer negotiate the sales contract (1), which calls for payment by letter of credit against specified documents. The contract should include a description of the goods, the amount, the unit price, the time allowed for shipment and presentation of the documents, the currency, the method of payment, and the terms of delivery.

Procedure Used in a Letter of Credit

Credit

Applications

Advising/Confirming bank

The foreign buyer informs the issuing bank of its requirement for a letter of credit in favor of the exporter using the issuing bank's application for a letter of credit and agreement forms. These forms constitute the payment and reimbursement contract between the foreign buyer and the issuing bank. The application (2) also serves as the foreign buyer's instruction to the issuing bank as to the terms and conditions of the letter of credit. These terms and conditions should ensure that the letter of credit's documentary requirements track, as closely as practically possible, the exporter's obligations under the commercial contract in terms of mode and timing of shipment, insurance coverage, invoice and certification requirements, etc. Before issuing the letter of credit, the issuing bank will require the foreign buyer to meet its credit requirements for the establishment of the letter of credit. This is because the issuing bank must pay the letter of credit regardless of whether the foreign buyer is able to reimburse it at the time of payment.

The issuing bank then sends the letter of credit (3) to the advising bank, which checks the apparent authenticity of the letter of credit. The advising bank then advises (4) the exporter of its receipt of the letter of credit, and the documentary requirements of the letter of credit. Upon receiving the letter of credit, the exporter checks out the credit's terms and documentary requirements to ensure that it is sufficient to meet the foreign buyer's payment obligations and that the required documents can be supplied in the time allowed. If the credit is insufficient in amount, or calls for documents that the exporter will not be able to supply before the credit's expiry, the exporter must have the foreign buyer instruct its bank to amend the letter of credit.

If the letter of credit is acceptable, the exporter ships the merchandise (5) to the foreign buyer. Payment is processed under the letter of credit upon presentation by the exporter of the required documents (6) to the advising bank. The advising bank then examines the documents to ensure that they appear, on their face, to meet the terms and conditions of the letter of credit. If the documents are in order, the advising bank (if nominated to pay/negotiate the letter of credit, and prepared to do so) informs the issuing bank and arranges for payment (7) to the exporter upon the receipt of funds from the issuing bank. (If the bank receiving the documents from the exporter was a "confirming bank," payment would be made to the exporter upon the confirming bank's determination that the documents were in order.) The issuing bank receives the documents (8) from the negotiating/paying bank, checks them for compliance with the credit, and then sends payment (9) to the advising bank. The issuing bank then presents the documents (10) to the foreign buyer to be reimbursed for its payments (11) under the letter of credit. The foreign buyer takes the shipping and title documents provided to claim the goods upon their arrival.

Information requirements of a letter of credit

The applicant must provide certain information to the issuing bank for incorporation in the letter of credit. The application for a letter of credit should include:

1. The full and correct name and address of the beneficiary (the Koreanexporter);

2. The designated bank of the Korean exporter;

3. The amount of the credit and its currency code;

4. Whether the credit is revocable, irrevocable, or irrevocable with therequested confirmation of the nominated (Korean) bank;

5. Whether the credit is to be available by payment, deferred payment,acceptance, or negotiation;

6. The party on whom drafts are to be drawn, and the tenor (time period)of the drafts;

7. A brief description of the goods, including details of quantity and unitprice;

8. Details of the documents required, with the express indication of the typeof transport document required;

9. Where the goods are to be shipped from and the place of final destination,or the port of discharge;

10. Whether freight is to be prepaid or collect;

11. Whether transshipment is allowed;

12. Whether part shipments are allowed;

13. The last date for shipment;

14. The period of time after shipment allowed for the presentation of documents;

15. The expiry date of the credit and the place for presentation of documents;

16. Whether the credit is to be a transferable credit;

17. How the credit is to be advised, i.e., by mail or by electronic communication;

18. Additional conditions, if any, in documentary form; and

19. Who is responsible for paying bank charges outside those of the issuingbank.

Routine users of letters of credit can often remit their instructions regarding the establishment of a letter of credit to their bank by personal computer. As such, applicants can re-create repetitive letters of credit and make changes such as dates, amounts, and quantities without rewriting the entire letter of credit. This allows applicants to reduce letter of credit preparation time and increase the accuracy of applications.

Forms of Letters of Credit

Letters of credit vary in form, and accordingly provide greater and lesser amounts of payment security. In particular, letters of credit may be:

• irrevocable or revocable;

• restricted or (freely) negotiable;

• advised or confirmed; and

• available by sight payment, by deferred payment, by acceptance, or bynegotiation.

Irrevocable versus revocable

An irrevocable letter of credit may not be modified, amended, or cancelled without the expressed consent of the issuing bank, the confirming bank (if any), or the beneficiary. It constitutes a definitive engagement of the issuing bank to honour the letter of credit provided that the documentary and other conditions have been met. By contrast, a revocable letter of credit may be modified, amended, or cancelled by the applicant via the issuing bank without the beneficiary's consent, by giving notice to the banks involved at any time up to the payment of the letter of credit. Because a revocable letter of credit leaves the exporter exposed to the risk that the buyer may decide not to pay for the goods, revocable letters of credit are used primarily between affiliated companies and not between unrelated companies. Under UCP 500, letters of credit are deemed to be irrevocable unless the letter of credit clearly states they are revocable.

Restricted versus negotiation

A restricted letter of credit limits the payment obligation of the issuing bank to the named paying bank. A negotiation letter of credit provides that the letter of credit may be negotiated by the nominated advising bank and that the issuing bank's engagement to pay will be extended to third parties negotiating the credit on behalf of the issuing bank. Unless specifically indicated otherwise, all letters of credit are negotiation letters of credit.

Advised versus confirmed

An advised (unconfirmed) letter of credit involves the advising bank informing the beneficiary that it is passing on the issuing bank's letter of credit without any engagement on its own part. The role of the advising bank is to take reasonable care to ensure that the credit appears to be authentic.2 Unless it has added its confirmation to the credit, the advising bank has no obligation to the beneficiary to pay, accept, or negotiate drawings. However, it may choose to assume the nominated role upon presentation of documents in order to pay the beneficiary. Negotiations under unconfirmed letters of credit are usually with recourse to the beneficiary.

Confirmation of the letter of credit involves the confirming bank taking on the same engagement as the issuing bank. As such, the confirming bank engages to pay the beneficiary upon the presentation of acceptable documents in compliance with the conditions of the letter of credit. This payment is without recourse to the beneficiary. Further, the confirming bank's engagement to pay

Fraudulent letters of credit are a well-known fact of life among bank personnel processing letters of credit. It is clearly prudent to ensure that letters of credit received by the exporter from unfamiliar foreign buyers are examined by bank personnel for authentication before any costs are incurred on the part of the exporter.

Letters of Credit

The beneficiary stands even if the issuing bank is unable to honor its commitment to reimburse the confirming bank. Exporters can use Korean bank confirmation of a foreign bank issued letter of credit to avoid the risk of non-performance by the foreign bank (whether due to the bank's own failure or country risks that prevent the bank from honouring its letter of credit). However, the request that a Korean bank add its confirmation to the issuing bank's letter of credit must come from the issuing bank (upon the instructions of the foreign buyer). A Korean bank cannot add its formal confirmation of a letter of credit — or secure its right to reimbursement from the issuing bank—without being asked to do so by the issuing bank.

However, it is occasionally possible for a Korean exporter to obtain a so-called "silent confirmation" whereby the Korean bank will agree to honour the letter of credit whether or not the issuing bank is able to honour its obligations. This silent confirmation is not a true confirmation per se, but rather a side agreement between the exporter and the Korean bank. It does not establish the rights of a confirming bank on the issuing bank. Silent confirmations tend to be used in circumstances where the issuing bank does not allow its letters of credit to be confirmed, but where the risks involved are such that the exporter needs the protection of a Korean bank confirmation. Where confirmation of the letter of credit by a Korean bank is not possible, export credit insurance may be available to cover the risks of non-payment. This may be used in circumstances where the confirming bank does not have adequate country risk appetite for the foreign buyer's issuing bank.

Payment options

Letters of credit can be available by demand payment, sight payment, deferred payment or usance, acceptance, or negotiation. Both demand and sight payments call for immediate value being given to the beneficiary upon satisfaction of the terms and conditions of the letter of credit. However, in The Republic of Korea, three days of grace are added to sight payments unless otherwise stated. Deferred payment calls for payment by the paying bank at a determinable future date without the presentation of a draft. Notably, the presentation of drafts is avoided in countries where there is a high stamp duty levied on the instrument. An acceptance credit calls for a nominated bank to accept drafts drawn on the confirming, issuing bank, or another drawee bank upon presentation of acceptable documents. Negotiation means the giving of value to the exporter for drafts and/or documents presented to the negotiating bank in compliance with the terms of the letter of credit. Negotiation with the issuing or confirming banks calls for payment, without recourse, to the drawers and/or bona fide holders of the draft.

Special Features of Letters of Credit

There are many special features of letters of credit that can be very useful to both Korean exporters and their foreign buyers. Such features include acceptance financing, partial shipments and red clause credits, transferable, assignable and back-to-back credits, standby credits, and revolving credits.

Acceptance financing

Letters of credit often call for the acceptance of term drafts by the advising, confirming, or issuing banks. In essence, term drafts provide the foreign buyer with financing for the period of time that the goods are held in the channels of trade (typically 30 to 180 days). These term drafts may be held until maturity by the exporter. If so, the exporter is providing, with the guarantee of the accepting bank, financing for the transaction. These drafts, called "bankers' acceptances," can also be discounted by the exporter at a bank and re-sold in the financial marketplace.

The discount rate for bankers' acceptances depends on the currency of the draft, perceived creditworthiness of the issuing bank, the term provided, the amount of the draft, and the issuing bank's country rating. As such, very competitive trade financing can be obtained from discounting bankers' acceptances. The exporter can also arrange to receive the face value of the accepted draft by having the credit stipulate that "discount charges are for the account of the buyer." In this case, the buyer pays the trade financing charges directly instead of through a higher export sales price.

Working capital relief to the exporter

Partial shipments and drawings, installment shipments and drawings, and red clause credits are all means of providing working capital relief to the exporter through a letter of credit. In the case of partial shipments, the exporter can ship and receive payment for a portion of the total supply order covered by the letter of credit. This frees the working capital being held in that portion of the supply order that has already been completed and made ready for shipment. Under UCP 500, partial shipments and drawings are allowed under a letter of credit unless specifically stated otherwise.

Installment shipments and drawings provide for a large sales contract being paid through a single letter of credit to be divided into smaller portions for completion, shipment and payment. This allows the export sale to be broken into more manageable portions by the exporter, and so eases total pre-shipment financing requirements. However, if installment shipments and drawings within given periods are stipulated in the letter of credit and an installment and/or drawing for a given period is missed, the letter of credit may not be used for any subsequent shipments and drawings without amendment.

Red clause credits are letters of credit that contain a clause (often printed in red) authorizing the paying bank to make advances to the exporter with which to purchase the goods to be shipped under the letter of credit. These advances are deducted from the amount due to be paid when the documents called for are presented. If the exporter fails to ship the goods, or cannot do so before the expiry of the letter of credit, the issuing bank is required to reimburse the paying bank. The issuing bank then looks to the foreign buyer to recover its payments.

Transferable credits, assignment of proceeds, and back-to-back credits

Transferable credits, assignments of proceeds, and back-to-back credits are used by exporters to share the proceeds of their letter of credit with their supplier(s). Each of these credits has special features that govern its use. A transferable credit involves the first beneficiary (the exporter) assigning the right to perform, and receive payment, under the original letter of credit to a second beneficiary (a supplier). An assignment of proceeds involves the exporter assigning a portion of its proceeds under the letter of credit to a supplier, but not its right to perform. The back-to back credit involves the exporter using the original letter of credit as collateral for the issuance of a second letter of credit in favor of the supplier. This last facility is not usually encouraged by banks.

Transferable letters of credit

A letter of credit can be transferable only if it is expressly designated as "transferable" by the issuing bank on the instruction of the applicant (foreign buyer). The transfer is of the first beneficiary's rights under the letter of credit to one or more second beneficiaries. That is, the second beneficiary obtains the right to present drafts and documents and to make demand for payment. Consequently, the first beneficiary's transfer of a portion of the letter of credit to a second beneficiary can result in the foreign buyer receiving goods from an unknown supplier.

At the time of making a request for transfer, the first beneficiary must instruct the transferring bank whether to advise the secondary beneficiary(ies) of amendments to the letter of credit. Further, if the letter of credit is transferred to more than one second beneficiary, refusal of an amendment by one second beneficiary does not prevent another second beneficiary from accepting the amendment. The letter of credit will remain unamended for second benefici-ary(ies) who rejects the amendment.

A transferable credit can be transferred only once. Consequently, the letter of credit cannot be transferred from a second beneficiary to a third beneficiary. Transfer of the letter of credit to more than one second beneficiary (as referenced above) is allowed, provided partial shipments and drawings are allowed, with the aggregate of such transfers being considered as only one transfer. The retransfer of the letter of credit back to the first beneficiary from the second beneficiary (ies) is also allowed.

The credit can be transferred only on the terms and conditions specified in the original credit except for the amount of the credit, any unit price stated in the credit, the expiry date, the last date for presentation of documents, and the period of shipment. Each of these items can be reduced or shortened to allow the first beneficiary to substitute its own invoices and prices, and demand for payment up to the difference between the original credit and the aggregate of the demands made by the second beneficiaries. Charges in respect to the transfer of the credit to the second beneficiary (ies) are for the account of the first beneficiary unless otherwise stated.

Assignment of proceeds under letters of credit

The foreign buyer may refuse to make the letter of credit transferable to safeguard its interests against commercial non-performance by unknown suppliers. Even so, the exporter can still assign its proceeds under the letter of credit to its suppliers. This assignment serves as collateral for suppliers who wish to secure their claim to payment from the exporter for goods supplied to the exporter for sale to the foreign buyer. In this regard, assignment of the letter of credit refers to the assignment of proceeds and not the assignment of the right to present documents and be paid under the letter of credit.

Assignment of the exporter's proceeds under the letter of credit should be by an irrevocable written instruction to the paying bank. These instructions should oblige the exporter to present the documents and drafts required by the letter of credit. The paying bank should then advise the assignees (the exporter's suppliers) of the assignment and the paying bank's agreement to pay out the proceeds accordingly. However, the paying bank should also advise the suppliers that the assignment of proceeds under the letter of credit does not constitute an irrevocable undertaking of the paying bank to pay the suppliers for goods supplied to the exporter. This is because the exporter may not be able to meet all of the terms and conditions for payment under the letter of credit.

Back-to-back letters of credit

There are no letters of credit with a back-to-back clause, per se. Rather, the term back-to-back letters of credit involve an exporter (who is the beneficiary of a letter of credit established by a foreign buyer) using the first letter of credit as collateral for the issuance of a second letter of credit in favor of its supplier. Back-to-back credits are used when the first letter of credit cannot be transferred to the exporter's suppliers, or when an assignment of the exporter's proceeds under the first letter of credit is considered insufficient security of payment for the supplier(s).

Back-to-back letters of credit are somewhat problematic. There is no guarantee that, once the beneficiaries of the second letter of credit have presented their documents and been paid, the exporter will also be able to meet all of the terms and conditions of the original letter of credit and be paid. If the exporter is unable to be paid under the first letter of credit, then the second issuing bank (which had relied on the exporter's assignment of its proceeds from the first letter of credit for reimbursement) will have to pursue its claim against the exporter for payment in other ways.

To minimize the likelihood of the exporter not being able to meet the terms and conditions of the first letter of credit, the second letter of credit should require that the suppliers produce the same documents (except the exporter's commercial invoice) as required by the first letter of credit, in sufficient time to enable the exporter to present them before the expiry of the first letter of credit.

Standby letters of credit

A standby letter of credit can be used to guarantee performance by the applicant (the exporter, in this case). As such, a standby letter of credit represents an obligation to the beneficiary (the foreign buyer, in this instance) on the part of the issuing bank to pay amounts owed by the exporter to the foreign buyer because of non-performance under the commercial contract.

Standby letters of credit are typically used as advance payment guarantees for down payments received by the exporter and as performance guarantees under commercial contracts. Usually simple demand - - without proof of non-performance by the exporter — is all that is required by the foreign buyer to receive payment under a standby letter of credit. As such, exporter protestations that performance has been rendered cannot stop the payment of the letter of credit.

Standby letters of credit can also be used to protect the exporter from the buyer's non-payment of recurring shipments. Here, the exporter desires the extra payment security afforded by letter of credit terms, but the foreign buyer and exporter wish to minimize banking and administrative costs. To accomplish both goals, the exporter and the foreign buyer can agree to: (1) the shipment of goods on open account terms (where title is transferred immediately to the buyer and the buyer remits payment by cheque, draft, or bank transfer); and (2) the establishment of a standby letter of credit in favor of the exporter (which could be drawn down by simple demand if payment is not received within a specified period of time). As long as the letter of credit is never drawn down, banking costs are limited to the costs of establishing the single letter of credit without the incurrence of document checking, document discrepancy and credit amendment, and funds remittance costs.

Revolving letters of credit

Revolving letters of credit are, upon use, automatically renewed or reinstated without specific amendments to the letter of credit. These credits are particularly useful for continuing shipments of a particular nature by the exporter to the foreign buyer over a specified period of time. For instance, a revolving letter of credit can be established that provides for a payment to the exporter of up to $15,000 per month upon the presentation of specified documents for a period of six months. This letter of credit is effectively for a total sum of $90,000.

Revolving letters of credit can be irrevocable or revocable. They can also be "cumulative" or "non-cumulative." Cumulative letters of credit allow sums not drawn down in a particular period to be drawn down in subsequent periods. In non-cumulative letters of credit, sums not used in a particular period are no longer available.

Management of Letters of Credit

This section sets out key management issues on letters of credit, including advantages and disadvantages to their use, financial aspects of letters of credit and how to guard against inappropriate letter of credit terms and document errors.

Advantages and disadvantages of using letters of credit

There are several advantages and disadvantages to using letters of credit.

The advantages include the facilitation of export sales through the use of letters of credit, the worldwide legal standing of letter of credit payment obligations, and the expert bank examination of shipping and title documents, which takes place in letter of credit transactions.

In particular, letters of credit facilitate export sales by:

• providing an independent bank credit backing and a clear promise to pay;

• providing lower cost trade financing through banker's acceptances;

• increasing the value of the export transaction by reducing the level ofcredit risk; and

• transferring foreign bank and country risk through Korean bank confirmations.

Enhanced legal protection for export payments is gained through the various laws and regulations that govern the use of letters of credit worldwide, as well as through UCP 500, which clearly establishes the rights and obligations of the international banks processing letters of credit. Finally, expert bank checking of the shipping and title documents used in letter of credit transactions gives comfort that the export transaction conforms to established documentary standards.

The disadvantages of letters of credit fall largely in the administrative and financing costs associated with letters of credit, the administrative rigidity of bank processing of the credits, limited bank engagements with respect to the documents provided and examined, and the separation of the buyer's payment obligation from the seller's contractual performance. More particularly, letters of credit are costly to implement given the bank services rendered in establishing the credit, examining documents, dealing with discrepancies and amending the credit, and transferring funds. Also, because the banks are bound by UCP 500 and the various national laws governing letters of credit, banks require rigid adherence to the rules—with the result that payments can be delayed for goods that may have been supplied if letter of credit requirements are not complied with. However, even when the banks examine the various documents, they take no responsibility for documents that are not authentic or that fail to safeguard the buyer's interests under the credit. Finally, because banks pay against documents and not commercial performance, it is not possible for buyers to withhold payment when the goods shipped are not of acceptable quality or other specifications. For this reason, buyers must ensure that the documents stipulated in the letter of credit protect their interests through inspection documents, etc.

Financial aspects of letters of credit

There are a number of financial aspects of letters of credit that should be considered by exporters contemplating letters of credit for their export transaction. The presentation of acceptable documents under the letter of credit does not necessarily guarantee the immediate receipt of good value funds. Advised credits can require up to five business days, or longer, before the funds are received by the bank for the credit of the exporter or the bank is authorized to pay. Where the exporter is able to negotiate payment under an advised letter of credit, this payment may be reduced to cover the interest charges while the funds are in transit. The payment might also be made with recourse to the exporter, to cover the advising bank's risk of non-reimbursement from the issuing bank under an unconfirmed letter of credit.

Establishing a letter of credit can also be relatively expensive. While charges vary by bank and the factors involved, letter of credit charges often include a document handling fee of about $200, an ad valorem charge of .1% to .3% of the letter of credit, fees to amend the letter of credit and handle document discrepancies, and various administrative costs. As a result, the minimum charge for a letter of credit is about $350 with the usual charge about $500. Clearly, these charges make using letters of credit for smaller transactions of, say, less than $10,000, prohibitively expensive. The level of costs involved with letters of credit also suggests explicitly building them into the price of the goods or services being exported or, alternatively, negotiating to have the foreign buyer pay the costs directly.

Guarding against inappropriate terms and document errors

Exporters considering the use of letters of credit should visit their commercial bank's international trade centre. Estimates of non-compliant documents range as high as 80% for novice exporters while experienced exporters can reduce documentation problems to almost zero. Overwhelmingly, bank officers dealing with letters of credit (and exporter complaints regarding non-payment of their letters of credit) would prefer to educate the exporter in the use of letters of credit and their choice of documents. In fact, receiving incorrect documentation is usually a "lose-lose" situation for the bank and its customer. Substantial periods of time must be spent seeking corrections to non-compliant documents or amendments to letters of credit to allow their use. Not surprisingly, it is difficult to establish bank-customer goodwill while the customer goes unpaid from non-compliant documents.

To help avoid non-compliant documentation, exporters should seek expert advice on the terms and conditions that should be included (or excluded) in sales contracts that call for payment by letter of credit. In particular, care should be taken to avoid documents and conditions that are outside of the control of the exporter (such as foreign inspections or customs clearance documents4). The exporter should also review the pro forma letter of credit documentary requirements with a bank documentation officer to ensure that the terms and conditions can be met. A knowledgeable freight forwarder can also assist in lessening the documentation risks of the letter of credit transaction.

Upon receipt of the advice of the letter of credit from the advising or confirming bank, the following details should be checked on each letter of credit:

1. Whether the names and addresses of the applicant and the beneficiary are complete and spelled correctly;

2. That the letter of credit is irrevocable;

3. Whether the credit is confirmed, if required;

4. Whether the amount and currency of the letter of credit is acceptable;

5. Whether the shipping and expiry dates are acceptable, and whether thetime period for presentation of the shipping documents is sufficient (it ispreferable if the place of expiry is The Republic of Korea);

6. Whether partial shipments or transshipments are allowed;

7. Whether the bill of lading requirements are acceptable;

8. Whether the ports of shipment and destinations are specified correctly;

9. Whether the description of goods to be shipped is correct;

10. Whether the required documents can be supplied;

11. Whether the specified quality of goods is correct, and sufficient tolerances are allowed;

12. Whether the insurance specifications are acceptable in terms of amountsand risk covered; and

13. Whether the letter of credit is available in The Republic of Korea by payment, negotiation, or acceptance (preferable).

Dealing with non-compliant documents

When a review of the letter of credit reveals errors or calls for documents that cannot be furnished by the exporter, the exporter must request an amendment to the letter of credit. To do so, the exporter contacts the foreign buyer, advising of the need for an amendment to the letter of credit. The buyer so informs the issuing bank, which advises the advising (or confirming) bank of the amendment, which, in turn, advises the exporter of the amendment. The letter of credit is so amended when all parties have agreed to the proposed amendment.

Often, however, the exporter's inability to comply with the terms and conditions of the letter of credit becomes apparent only after the goods have been shipped and the documents produced and submitted to the bank for payment. For instance, the documents may be produced in error or shipment may have been delayed by bad weather beyond the last shipping date specified in the letter of credit. In such cases, the exporter can:

1. Attempt to have the documents corrected by the party producing them. Here it is necessary to have the documents ready for resubmission within the time requirements for the letter of credit.

2. If the documents cannot be corrected, have its bank request authorityfrom the issuing bank to negotiate the draft, despite the discrepancies.

3. Sign an indemnity with the paying bank whereby the exporter will repaythe bank for advances made under the letter of credit, if the issuing bankrefuses to accept the documents.

4. Send the documents to the issuing bank on an approval basis. Here thedocuments are to be delivered to the buyer only upon the buyer'sauthority to pay or accept drafts. Non-compliance under the letter ofcredit risks non-payment.

A closing note on letters of credit

Letters of credit are specialized international banking documents that provide a secure means of payment for international trade transactions. However, the rules governing the use of letters of credit are fairly rigid and the administrative costs relatively high. These factors call for the careful use of letters of credit.

Letters of credit also seem to be somewhat prone to fraudulent use. Numerous instances of bogus letters of credit, drawn on fictitious banks, have occurred. Likewise, the presentation of acceptable documents under a letter of credit does not guarantee the provision of acceptable goods. Clearly, it is important for the Korean exporter and the foreign buyer to know one another, and each party's capabilities, before entering into letter of credit arrangements.

Finally, the use of letters of credit ought to be considered in light of the firm's risk management policies and objectives. Indiscriminate use of letters of credit for small export transactions will likely lead to poor cost/benefit ratios. Smaller sales are likely better financed and risk managed using open account selling with the security of standby letters of credit, export credit insurance, or export receivables discounting.

Adapted from: Ross, D.G. (1998) Export Finance: A Guide for Canadian Managers, Carswell Thomas Professional Publishing.